jueves, 24 de enero de 2013

miércoles, 16 de enero de 2013

Signals Few good setups

Signals

Swing Play

pullback play

Swing Play

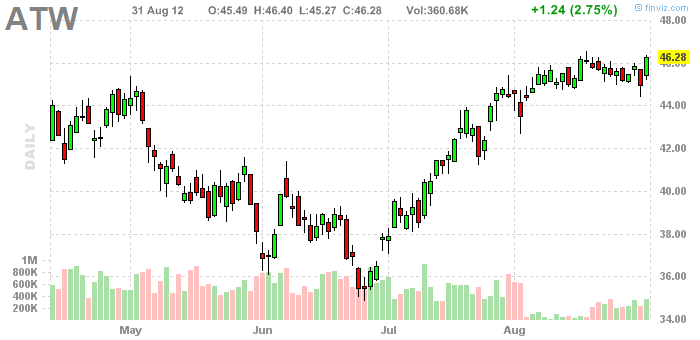

145 possible target

Swing Play

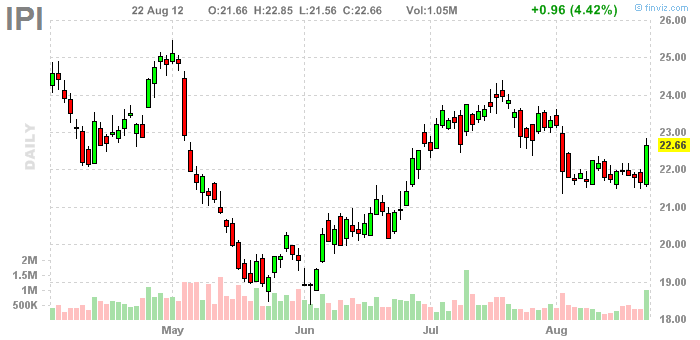

24.5 possible target.

Swing Play

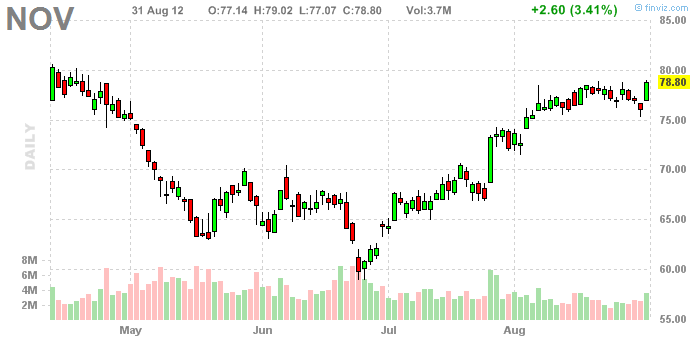

24 possible target

Stock To watch

Earnings last night.

martes, 8 de enero de 2013

Forex Swing trading opportunities

Forex

Several stocks are breaking out and there are some nice setups showing up in our scans. Many stocks are going sideways during market consolidation and are now breaking out.

lunes, 7 de enero de 2013

Forex Swing trade idea: RYL

Forex

RYL seems to be ready to head higher after 2 months sideways base for swing trade. 10 to 20% potential from here.

sábado, 5 de enero de 2013

Forex UYMG Issues Impressive News Today

Forex UYMG is a stock I posted last week as a bounce candidate. Today's news could help bolster investor sentiment. After posting some strong revenue numbers the president of UYMG stated:

Might not be a bad time to take a closer look at UYMG. I think the stock heads back over $.002 this week... but what do I know?

On Track Technology Begins Work On Production Leases In Navarro County

EAST HANOVER, N.J., Sept. 4, 2012 /PRNewswire via COMTEX/ -- Unity Management Group (OTC Pink:UYMG ), a business resource and service company, is pleased to announce its wholly owned subsidiary, On Track Technology Solutions Inc. (OTT), and their consulting firms have entered into a farm out agreement to begin work to establish production on a group of contiguous leases in Navarro County. There are approximately 52 wellbores with 6 being State approved injection wells; wellbores identified at the Texas Railroad Commission as lease numbers 01689, 02032, 02033, 02216 and 02503.

'Our authorized share count has risen this year to account for our transition into On Track Technology becoming our main subsidiary. We will not be raising the Authorized share count any further while we control/own UYMG,' said Michael Oliver president of Unity Management group Inc. He went on to add that our valuation or market capitalization is very low for the nature of what we are trying to accomplish. Our valuation is that of many OTC Market shell companies at this time. We are not a shell and have many results, announcements, and filings coming, that will yield a higher value immediately as traders and investors participate in the trading of our stock. We are looking for millions of dollars of value and business here, not 10s of thousands or hundreds of thousands.

Might not be a bad time to take a closer look at UYMG. I think the stock heads back over $.002 this week... but what do I know?

EAST HANOVER, N.J., Sept. 4, 2012 /PRNewswire via COMTEX/ -- Unity Management Group (OTC Pink:

OTT President, Eddie Schilb said, 'On Track is working with an area Geologist, and a Chemical firm to develop a confidential completion, and chemical Huff & Puff treatment using Co2, Nitrogen or a combination of the two. Based on conversations with one Petroleum Engineer we believe a potential of 89 BOPD may be achievable upon a successful implantation, and successful results of treatment, installation of proper production equipment, and pressurization of certain/specific wellbores within the leases. While the price of oil varies daily we used $86.08 per barrel (todays price although most 5 year forecast is $101.07 Per Barrel); upon successful implementation 89 BOPD would add approximately $186,318 per month or $2,235,821 annually.

On Track Vice President and Staff Engineer Ayo Odetunmibi commented that this property fits nicely with our other properties. 'We are looking forward to testing these wells; it is an exciting time and I am excited about the potential in this field. Eventually we want to test the possibility of other profitable formations on this acreage.'

'Our authorized share count has risen this year to account for our transition into On Track Technology becoming our main subsidiary. We will not be raising the Authorized share count any further while we control/own UYMG,' said Michael Oliver president of Unity Management group Inc. He went on to add that our valuation or market capitalization is very low for the nature of what we are trying to accomplish. Our valuation is that of many OTC Market shell companies at this time. We are not a shell and have many results, announcements, and filings coming, that will yield a higher value immediately as traders and investors participate in the trading of our stock. We are looking for millions of dollars of value and business here, not 10s of thousands or hundreds of thousands.

jueves, 3 de enero de 2013

Earn Hotel industry looks for deal pace to pick up

Earn LOS ANGELES (Reuters) - Hotel companies and real estate firms are optimistic that deal transactions will pick up this year despite concerns about Europe's economy and challenges in obtaining debt financing. While a business-led economic recovery has helped lift U.S. hotel occupancy rates, development is still a soft spot as tight credit conditions have limited new-hotel builds. Still, there is a growing sense that the hotel sector has momentum and performance will continue to improve. 'People are expecting 2012 to be a pretty positive year, with solid performance by the industry in terms of the demand for hotel accommodations and the ability to get deals done,' Arthur de Haast, chairman of Jones Lang LaSalle Hotels, said at this week's Americas Lodging Investment Summit. The hotel investment services firm has forecast that hotel deals in the Americas this year will at least match the 2011 level in value of an estimated $15 billion. U.S. hotel deal activity picked up in the first half of 2011 but calmed in the latter part of the year as debt woes in Europe began dominating the headlines. While Europe is still a risk, attendees at the three-day hotel conference said a continued recovery marked by rising room rates would make the sector attractive for investment. 'There's a lot of money on the sidelines waiting to pounce and find opportunities,' said Christian Charre, president and chief executive of the Charre Group, a Florida-based hotel brokerage and consulting firm. FOREIGN MONEY Private equity funds that have capital will be in a good position to make acquisitions, some said. Real estate investment trusts were active buyers in the first half of 2011 but are expected to be quieter this year as their share prices suffered in the latter part of 2011. 'The mix of the investors probably will change,' said Sri Sambamurthy, co-founder of real estate firm West Point Partners in New York. He said Middle Eastern, European and Asian investors especially find the U.S. market to be extremely attractive now. 'The U.S. is still considered very safe, the dollar has performed extraordinarily well,' Sambamurthy added. Hotel companies said they were looking to make acquisitions in a bid to expand their reach. 'No question that we'll be active in the marketplace in 2012,' said Paul Whetsell, president and chief executive of Loews Hotels, which owns and/or operates 18 hotels. The unit of Loews Corp (NYSE:L - News) has committed more than $500 million to acquiring hotels or developing new properties. Whetsell said Loews is looking for 4-star or higher-rated hotels in major cities where it does not have a presence such as Boston, Washington, San Francisco, Chicago and Los Angeles, as well as smaller markets like Charlotte, North Carolina, and Baltimore, Maryland. Choice Hotels International (NYSE:CHH - News), which franchises hotels focused mainly at the mid-tier and economy market segments under brands such as Comfort Inn and Econo Lodge, said it is in the hunt to acquire a value-oriented, full-service upscale brand that would help attract more business customers.

martes, 1 de enero de 2013

Earn For Europe, Few Options in a Vicious Cycle of Debt

Earn For Europe, Few Options in a Vicious Cycle of Debt Europe has a $1 trillion problem. As difficult as the last two years have been for Europe, 2012 could be even tougher. Each week, countries will need to sell billions of dollars of bonds - a staggering $1 trillion in total - to replace existing debt and cover their current budget deficits. At any point, should banks, pensions and other big investors balk, anxiety could course through the markets, making government officials feel like they are stuck in a scary financial remake of 'Groundhog Day.' Even if governments attract investors at reasonable interest rates one month, they will have to repeat the process again the next month - and signs of skittish buyers could make each sale harder to manage than the previous one. 'The headline risk is enormous,' said Nick Firoozye, chief European rates strategist at Nomura International in London. Given this vicious cycle, policy makers and investors are closely watching the debt auctions for potential weakness. On Thursday, Spain is set to sell as much as 5 billion euros ($6.3 billion) of government bonds. Italy follows on Friday with an auction of more than $9 billion. The current challenge for Europe is to keep Italy and Spain from ending up like Greece and Portugal, whose borrowing costs rose so high last year that it signaled real likelihood of default, making it impossible for the governments to find buyers for their debt. Since then, Greece and Portugal have been reliant on the financial backing of the European Union and the International Monetary Fund. The intense focus on the sovereign debt auctions - and their importance to the broader economy - starkly underscores the difference between European and American responses to their crises. Since 2008, there has been almost no private sector interest to buy new United States residential mortgage loans, the financial asset at the root of the country's crisis. To make up for that lack of investor demand, the federal government has bought and guaranteed hundreds of billions of dollars of new mortgages. In Europe, policy makers are still expecting private sector buyers to acquire the majority of government debt. Last month, in perhaps the boldest move of the crisis, the European Central Bank lent $620 billion to banks for up to three years at a rate of 1 percent. Some officials had hoped that these cheap loans would spur demand for government debt. The idea is that financial institutions would be able to make a tidy profit by borrowing from the central bank at 1 percent and using the money to buy government bonds that have a higher yield, like Spain's 10-year bond at 5.5 percent. But the sovereign debt markets continue to show signs of stress. Italy's 10-year government bond has fallen in price, lifting its yield to more than 7 percent, a level that shows investors remain worried about the financial strength of Italy's government. And European banks appear to be hoarding much of the money they borrowed from the central bank, rather than lending it to governments. Money deposited by banks at the European Central Bank, where it remains idle, stands at $617 billion, up from $425 billion just a month ago. 'It's hard to see why a banker would want to tie up money in a European sovereign for, say, three years,' said Phillip L. Swagel at the University of Maryland's School of Public Policy, who served as assistant secretary for economic policy under Treasury Secretary Henry M. Paulson Jr. Italy's troubles highlight how hard it is to generate demand for a deluge of new debt from a dwindling pool of investors. The country needs to issue as much as $305 billion of debt this year, the highest in the euro zone. By comparison, France, with the second highest total, needs to auction $243 billion of new debt, according to estimates by Nomura. Governments like Italy's are at the mercy of markets because they simply don't have the cash to pay off even some of their bonds that come due. They must issue new bonds to cover their old debts, as well as their budget deficits, at a time when investors are growing scarce. Banks, traditionally big holders of government bonds, have been selling Italian debt. 'We've seen a lot of liquidation by non-European investors,' said Laurent Fransolet, head of European interest rate strategy at Barclays Capital in London. For instance, Nomura Holdings in Japan slashed its Italian debt holdings, mostly government bonds, to $467 million on Nov. 24, from $2.8 billion at the end of Sept. European banks have also been dumping the debt. BNP Paribas, a French bank, cut its exposure to Italian government bonds to $15.5 billion at the end of October, from $26 billion at the end of June. Italian banks, though large owners of their government's obligations, may not want to take on too much more, to keep their investors happy. Shares in UniCredit have fallen more than 40 percent since last week as the Italian firm has tried to raise capital to comply with new regulations. There are ways to avoid spectacularly bad debt auctions, at least in the short term. The central bank can help by buying a country's bonds in the market ahead of a new debt sale. That would help bolster prices at the auction, or at least keep them stable. There is also some evidence that banks' government-bond selling may have abated at the end of last year, according to Mr. Fransolet. Central bank figures show European financial firms acquired $2.4 billion of Spanish government bonds in November, after selling a monthly average of $4.8 billion in the preceding three months. Governments may also be able to attract new buyers to their bond markets. Belgium sold $7.2 billion of government bonds to local retail investors last month, in part appealing to their patriotism. Opportunistic hedge funds, betting the market is too pessimistic about certain European countries, may also bite. Saba Capital Management, a New York-based hedge fund headed by the former Deutsche Bank trader Boaz Weinstein, owns Italian government bonds, though it does so as part of a wider trading strategy that includes bets that could pay off if Europe's problems worsen. But it is doubtful that Italy and Spain can find enough new buyers this year to bring their bond yields down to sustainable levels. Instead, if their economies slow - and if their governments become unpopular - debt auctions could fail and their cost of borrowing could rise even more. All eyes would then turn to the central bank for drastic action. It could lend more cheap money to banks, in the hope that some of it might find its way into government bonds. Or it could become a big buyer of government bonds itself, printing euros to finance the purchases. But that may not be a lasting solution, since the central bank's actions could scare off private investors. Typically, when government-backed organizations like the central bank hold a country's debt, their claims on the debtor rank higher than those of other creditors. For that reason, private investors might think their holdings would fall in value if the central bank became a big owner of Italian debt - and they might retreat. At the same time, the crisis response in the United States did not depend solely on government-backed entities like the Federal Reserve to buy housing loans. Professor Swagel of the University of Maryland points out that banks and investors also took large losses on existing housing debt. While painful, the mortgage debt proved less of a drag on the financial system. So far, Europe has been averse to taking permanent losses on government bonds. Except in the case of Greek debt, European policy makers have shied away from any plan that could mean private holders of government debt get hurt. However, Nouriel Roubini, a professor of economics at the Stern School of Business at New York University, recently argued in a Financial Times editorial that Italy's debt should be reduced to 90 percent of the gross domestic product from 120 percent. In such a situation, investors might suffer a 25 percent hit on the value of their Italian bonds, he said. Such haircuts might seem like the recipe for more instability right now. But if Europe struggles to find buyers for its debt, more radical options are likely to be considered. Europe's debt problem is huge, and the experience in the United States suggests dealing with it may take several, more drastic approaches. 'If you go halfway, you'll never get to the end,' Professor Swagel said. 'And that describes European policy-making.'

Oil Five Sub-Penny Charts To Watch

Oil At the start of 2012 I posted charts to watch heading into the year. All of them rose 150% or more: http://pennystockgurus.blogspot.com/2012/02/150-or-bust.html

With the year 67% over I have five charts to watch. I think all five will at some point post an over 100% gain from their current prices. The stocks are UYMG at $.001, ERBB at $.0021, STKO at $.001, ELRA at $.0012 and MCVE at $.03.

With the year 67% over I have five charts to watch. I think all five will at some point post an over 100% gain from their current prices. The stocks are UYMG at $.001, ERBB at $.0021, STKO at $.001, ELRA at $.0012 and MCVE at $.03.

Suscribirse a:

Entradas (Atom)